Save

Save Print

Print[Ferro-Alloys.com] Tshipi Q3 FY2024 Quarterly Activities Report

Jupiter Mines Limited (ASX. JMS) (Jupiter or the Company), and together with its subsidiaries, the Group, is pleased to provide the following activities report for the quarter ended 31 March 2024.

Jupiter has a 49.9% beneficial interest in Tshipi é Ntle Manganese Mining Proprietary Limited (Tshipi), which operates the Tshipi Manganese Mine in the Kalahari manganese field. All Tshipi information is reported on a 100% basis (not based on Jupiter’s 49.9% economic interest). References to quarterly periods for FY2024 are for the quarters ending 30 September, 31 December, 31 March and 30 June.

Tshipi Key Performance Indicators

Q3 production and sales in line with expectations for the financial year

Sales of 789,788 tonnes (3% increase on previous quarter, 16% decrease on prior year corresponding period (“PCP”))

Production of 749,598 tonnes (26% decrease on previous quarter, 11% decrease on PCP), noting record production in Q2

Cost of production US$2.21 per dmtu FOB (10% increase on previous quarter, 8% increase on PCP)

Zero LTIs in the quarter, TRIFR increased to 0.52 (last quarter: 0.30)

Quarterly Activities Report Summary

Tshipi sales on track to achieve expected financial year volumes of 3.3Mt to 3.4Mt of shipped ore.

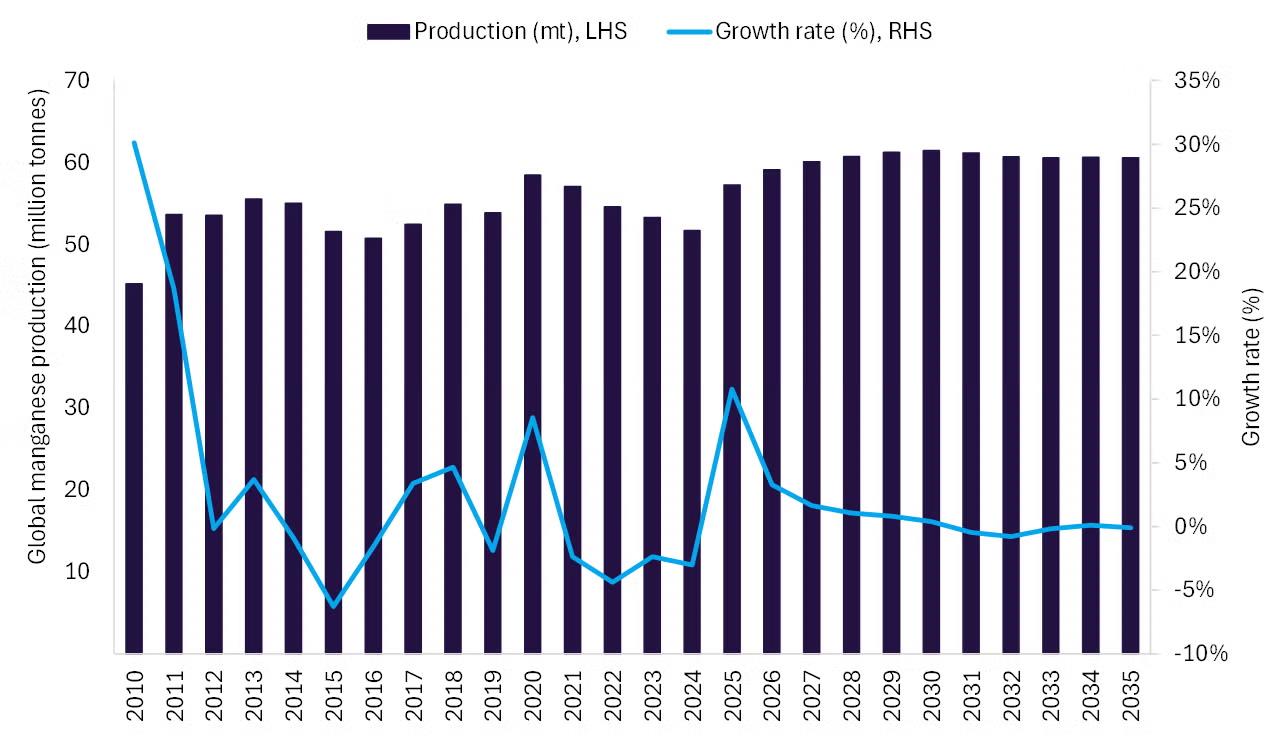

The March 2024 quarter saw spot manganese ore prices rise from six-year cyclical low levels seen in the December 2023 quarter. The average spot price (US$/dmtu, 37% FOB) for the March 2024 quarter was US$2.97, compared with an average of US$2.77 for the December 2023 quarter. The spot price at the end of the quarter (2 April 2024) was US$3.04. Notwithstanding improvements during the quarter, March 2024 spot prices were low compared to historical averages (see below).

Post quarter end, manganese ore prices have sharply increased due to concerns around supply shortages. This was driven by cyclone damage to GEMCO, a manganese mine in Australia that supplies approximately 12% of all manganese to the market. As at 29 April 2024, the benchmark spot price (US$/dmtu, 37% FOB) had risen to US$3.92 (+29% month on month movement). Given the materiality of GEMCO to global manganese supply, Jupiter expects manganese ore prices to continue to be supported in the near term. South 32 (GEMCO’s 60% owner) recently stated that they expect normal production to be restored in the March 2025 quarter (preliminary estimate), with the possibility of earlier, partial, ore export capability.

This March 2024 quarterly includes revenue and associated earnings based on sales prices agreed with customers during the November 2023 to February 2024 period, when manganese ore prices were low. The improved spot prices observed post quarter end will benefit Tshipi’s revenue from the month of June 2024.

Notwithstanding the sharp increase in spot ore prices in April 2024, the current price of US$3.92 is only slightly above the 6-year average of US$3.88. For comparison, the six-year high price (April 2020) was US$6.31 and the six-year low price (November 2019) was US$2.52. Tshipi’s earnings are sensitive to the manganese price: every US$1/dmtu increase (for 12 months) results in ZAR 1.8 billion of additional EBITDA (approximately A$146 million).

Key production, sales and financial information for Tshipi for the quarter ended 31 March 2024 and comparatives are presented below:

|

Key Statistic |

Unit |

Q3 FY2024 |

Q2 FY2024 |

Q1 FY2024 |

YTD FY2024 |

Q3 FY2023 |

|

Production |

Tonnes |

749,598 |

1,015,633 |

786,308 |

2,551,539 |

844,375 |

|

Sales (including mine gate sales) |

Tonnes |

789,788 |

764,162 |

928,361 |

2,482,311 |

945,154 |

|

Average CIF price achieved (HGL) for sales concluded on a CIF basis (see note 1) |

US$/dmtu |

3.55 |

3.47 |

3.64 |

3.64 |

4.28 |

|

Average FOB price achieved (HGL) for sales concluded on an FOB basis (see note 1) |

US$/dmtu |

2.80 |

2.89 |

2.91 |

2.87 |

3.64 |

|

Average FOB cost of production (HGL) |

US$/dmtu |

2.21 |

2.00 |

1.95 |

2.07 |

2.04 |

|

Earnings before interest, tax & depreciation (EBITDA) |

A$ million |

15.5 |

13.0 |

32.7 |

61.2 |

73.0 |

|

Net profit after tax (NPAT) |

A$ million |

10.4 |

10.2 |

22.2 |

42.8 |

50.2 |

|

Cash at bank |

A$ million |

70.3 |

92.6 |

128.3 |

70.3 |

84.4 |

Note 1

Tshipi sells most of its ore on a CIF basis. See “Logistics and Sales” below for a full breakdown.

SAFETY AND ENVIRONMENT

Tshipi recorded no lost time injuries (“LTIs”) during the quarter. TRIFR increased to 0.52 for the quarter (previous quarter 0.30).

MINING AND PRODUCTION

|

|

Unit |

Q3 FY2024 |

Q2 FY2024 |

Q1 FY2024 |

YTD FY2024 |

Q3 FY2023 |

|

Mined volume |

|

|||||

|

bcm |

3,089,486 |

3,091,027 |

3,475,354 |

9,655,867 |

2,468,796 |

|

bcm |

154,398 |

180,837 |

179,172 |

514,407 |

229,882 |

|

Total |

|

3,243,884 |

3,271,864 |

3,654,526 |

10,170,274 |

2,698,678 |

|

Production |

|

|

|

|

|

|

|

Tonnes |

651,155 |

815,689 |

662,009 |

2,128,853 |

720,027 |

|

Tonnes |

98,443 |

199,944 |

124,299 |

422,686 |

124,348 |

|

Total |

|

749,598 |

1,015,633 |

786,308 |

2,551,539 |

844,375 |

|

Average FOB cost of production (HGL) |

US$/dmtu |

2.21 |

2.00 |

1.95 |

2.07 |

2.04 |

Waste mining was in line with the previous quarter, while mining of graded ore was down 15% compared to the previous quarter. This was mainly due to the section of the pit that was predominantly mined during the quarter, being less productive than other areas (higher strip ratio). The mining sequence has been amended to allow for catch up over the remainder of the financial year. Heavy rainfall also interrupted production for a two-week period during March 2024.

Production volumes decreased 26% from the previous quarter, noting that Tshipi achieved record production in the previous quarter.Further, minimal low-grade ore was produced due to market conditions. Production remains on target on an annualised basis and healthy stockpiles remain to fulfill exports.

Cost of production on an FOB basis increased 10% on previous quarter. This was expected and was due to a combination of the increased costs of mining the section of the pit that was predominantly exploited during the quarter, combined with a (related) lower production of high-grade ore (which commensurately increased the unit cost of production).

- [Editor:tianyawei]

Daily News

Daily News Research

Research Magazine

Magazine Company Database

Company Database Customized Database

Customized Database Conferences

Conferences Advertisement

Advertisement Trade

Trade

Online inquiry

Online inquiry Contact

Contact

Tell Us What You Think